As you move through your career, it’s easy to forget about old retirement accounts.

You can take control of your retirement savings with a rollover IRA.

A rollover IRA is an “Individual Retirement Account” that lets you move money from a 401(k) or other employer plan into your own IRA without paying taxes or penalties, as long as you follow the rules. It allows you to keep your savings in one place, where they can potentially grow tax-deferred, and you can continue contributing to it.

The rollover process typically begins when you open an IRA and transfer your employer plan account to your new IRA account. If you roll to an IRA with Principal®, the process is more streamlined because it’s transferring with the same service provider as your 401(k) plan. The money is automatically moved.

Open an IRA

Contact your old 401(k) service provider

Check gets mailed

Money deposited into IRA

If you move your 401(k) to an IRA at the same company, the process is pretty simple. You open the IRA, and the money is moved straight from your 401(k) to the new account—no check is needed.

We help make it easy to roll over, easy to manage, and we’re here for you when you need it.

A rollover IRA can help simplify your savings while giving you control and a range of investment choices.

With IRAs, you are no longer subject to your former employer’s plan features. You are subject to IRS rules regarding any applicable taxes or penalties.

In an IRA, you can continue to make contributions and rollover other past employer retirement plans into your IRA.

IRAs generally have more investment options and are not limited to the investments selected by your former employer.

If the money from your 401(k) plan goes directly into your new IRA, you won’t owe any taxes. This is called a direct rollover. Rolling from your employer plan serviced by Principal to an IRA with Principal is an example of a direct rollover. If the money is sent to you first, you generally have 60 days to move it into another retirement account. If you miss that deadline, the distribution will be taxable and you may also be subject to an early withdrawal penalty.

- If your rollover is going to an IRA outside of Principal, the money is usually sent by check through the mail. The process typically takes 2-4 weeks to complete, but depends on mail delivery and the receiving IRA provider’s processing timeline.

- If you open an IRA with Principal, the process is typically faster. The form takes about 10 minutes to complete, and your money should show up in the new IRA in 7 to 10 days after it’s processed. You can keep using your current username and password.

There are several reasons people may choose to move their 401(k) into an IRA:

- More investment options: IRAs usually offer more choices, such as stocks, bonds, mutual funds, and ETFs. In a 401(k), your employer determines which investments are available to you.

- Possibly lower administrative fees: IRAs often have lower administrative fees than 401(k) plans. Some 401(k)s also charge a fee each time you take money out. When considering an IRA be sure to take into consideration the investment fees and expenses compared to those of the 401(k) plan.

- Greater control: You choose where to keep your IRA and how to invest your money since it’s no longer tied to the decisions of your former employer.

- Easier to manage: You can combine several old 401(k)s into one IRA, which can make it easier to track your savings and possibly reduce account maintenance costs, and help you see a clearer picture of your progress toward retirement.

Yes. After your rollover, you can continue to contribute to your IRA, as long as you meet the IRS rules.

- Traditional IRA: You can contribute if you have earned income. There is no income limit, but the IRS does set a yearly dollar limit.

Deductibility of contributions is dependent upon coverage by an employer-sponsored retirement plan for you or your spouse and your Modified Adjusted Gross Income (MAGI). - Roth IRA: These have income limits. If your income is too high, you may not be able to contribute directly.

Yes, you can withdraw money from your IRA, but there are important rules to understand:

- Traditional IRA: You can take out money without a penalty starting at age 59½. The IRS requires you to start withdrawing money by age 73. If you withdraw early, there may be a 10% penalty, unless you qualify for certain exceptions.

- Roth IRA: You can take out your contributions (the money you put in) at any time, without a penalty. You can withdraw your earnings tax- and penalty-free once you reach age 59½ and have had the account for at least five years. You can also withdraw money penalty-free at any age if you qualify for certain exceptions. These exceptions are the same as those for Traditional IRA. Unlike traditional IRAs, Roth IRAs do not require minimum distributions at any age.

This varies across employer plans and by retirement plan service providers. Some service providers charge a distribution fee to close your retirement plan account and process the rollover. If the service provider charges a fee, it generally applies whether you roll to an IRA, move to a new employer’s plan, or cash out the account.

Every IRA provider is different, but there are generally a few potential costs for an IRA that involve one or more of the following types of expenses:

- Expense ratios. Every mutual fund has an expense ratio because there are general costs associated with managing the fund. This expense is calculated in terms of a percentage. Always review the investment expense for each investment option selected.

- Transaction fee. A fund may have a fee for purchasing, selling or may not have any fee at all. (Sometimes these are known as “loads” of a fund.)

- Account maintenance fee. IRA providers may charge an annual cost for managing the account. Some providers waive the fee for account balances over a certain amount, such as when there’s $10,000 or more in the account.

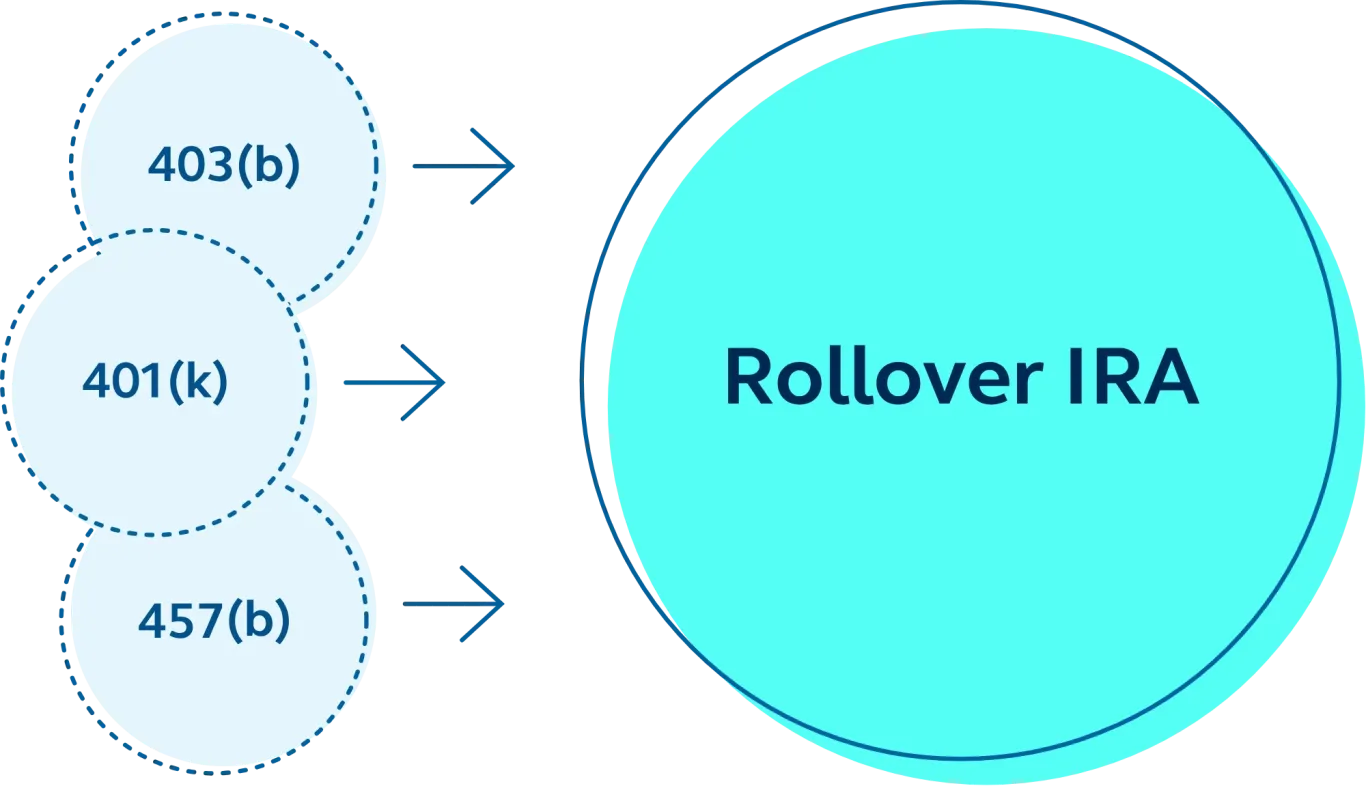

If you’re moving money from a 401(k), you’re usually putting it into a rollover IRA. This type of IRA lets you keep your retirement savings in one place and still get the same tax benefits. A rollover IRA is meant to hold money from other retirement accounts. It can be either a traditional IRA or a Roth IRA.

When you roll your 401(k) account from a plan serviced by Principal into an IRA with Principal, your money automatically goes to the right type of account based on your 401(k):

- Pre-tax (traditional) money goes into a Traditional Rollover IRA.

- Roth (after-tax) money goes into a Roth Rollover IRA.