As Social Security approaches a funding crossroads, policymakers face choices that could affect benefits, taxes, and retirement confidence. This article breaks down the realities behind the headlines and explores how potential reforms may impact workers, retirees, and employer-sponsored plans.

Few retirement topics generate as much conversation, concern, and confusion as Social Security. Headlines regularly warn of insolvency, benefit cuts, or a system “on the brink,” leaving plan sponsors and financial professionals navigating a stream of questions from plan participants.

The reality is more nuanced. Social Security isn’t going bankrupt and the truth is, benefits will continue to be paid, even if Congress takes no action. But the program is facing a well-documented financing gap that lawmakers must eventually address. How that gap is closed will have real implications for retirement planning, workforce strategies, and participant retirement readiness.

Social Security operates as a pay as you go system, funded primarily by payroll taxes collected from workers and their employers (or directly by self-employed individuals). Today’s workforce pays for benefits for today’s retirees. Contrary to a common belief, workers are not setting aside their own individual contributions for later withdrawal; rather, payroll taxes are pooled to fund current obligations.

When payroll tax revenue falls short, the program draws on reserves from the Social Security Trust Fund (which consists of two accounts: one for old age and survivor benefits and one for disability benefits).

Over time, that balance has shifted. An aging population, longer life expectancies, and fewer workers supporting each retiree mean more benefits are paid out than payroll Social Security taxes bring in each year.

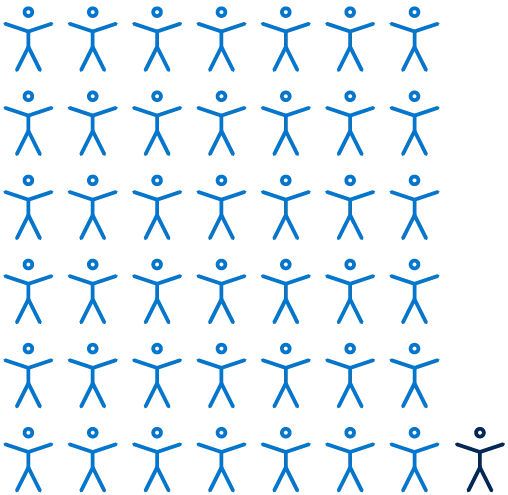

In 1945 there were 42 workers paying into the system per beneficiary receiving benefits. By 2035 the ratio is expected to drop to 2.4 workers per beneficiary.

1945

2035

For illustrative purposes. Social security and Medicare Boards of Trustees, 2024 Annual Report.

As a result, the program has been drawing down the reserves in the Trust Fund. According to the Social Security Trustees, those reserves are projected to be depleted by 2033, contributing to an estimated $25 trillion long term shortfall over the next 75 years.

The important thing to understand is that depletion doesn’t mean Social Security stops paying benefits. Even without congressional action, the program would continue collecting payroll taxes and paying benefits. The issue is not whether benefits continue — it’s whether full benefits can be paid under current law.

If Congress takes no action, benefits would automatically be reduced to match incoming revenue, resulting in an across the board cut of roughly 23%–25% for all beneficiaries.

That reduction would have serious consequences because so many Americans rely on Social Security as a primary source of retirement income. Nearly 40% of seniors depend on Social Security for all their income, and roughly 66% rely on it for at least half of their retirement income.

For plan sponsors, this financial gap matters because it can directly influence participant behavior and retirement outcomes. Reduced confidence in Social Security may lead workers to delay retirement, depend more heavily on employer sponsored plans to make up potential income shortfalls, or underestimate the income they may need from workplace savings. As a result, employer retirement plans play an even more important role in helping participants bridge potential income gaps and build sustainable retirement strategies beyond Social Security alone.

Employee confidence in receiving Social Security to pay for retirement expenses fell sharply from 61% in 2023 to just 46% in 2025. A decline driven primarily by younger workers, as only 24% of Gen Z and 35% of Millennials expect government programs to play a meaningful role in funding their retirement.

In 2026, the Senate Budget Committee held hearings to examine the solvency challenge and discuss potential paths forward. Committee members from both sides of the aisle agreed that addressing Social Security’s long term funding gap will almost certainly require a combination of changes rather than a single solution. To restore sustainability, lawmakers emphasized the importance of leveraging three broad levers: revenue, benefits, and program structure.

Below are commonly discussed approaches, each with different implications for workers, employers, and retirees.

Raising or eliminating the earnings cap. Today, workers and employers each pay a 6.2% Social Security payroll tax on earnings up to an annual limit, known as the taxable wage base. In 2026, that cap is $184,500, meaning earnings above that amount are not subject to the Social Security portion of payroll taxes (nor do they generate earned Social Security benefits).

When Social Security was created, about 90% of all wages were taxed; today, only about 80–85% are, largely because earnings above the cap have grown much faster than typical wages.

Advocates for raising the earnings cap believe this would restore Social Security’s original financing intent. Opponents of the idea believe raising the earnings cap without a corresponding increase in benefits breaks the “earned benefits” link of Social Security.

Increasing payroll rates. Another approach, often described as “modestly increasing contribution rates over time,” involves small, incremental increases to the payroll tax rate (for both employees and employers), typically measured in tenths of a percentage point and phased in gradually over many years. For example, a total increase of 1 percentage point over a decade would raise the combined employee-and-employer tax rate from 12.4% to 13.4%, limiting the immediate impact on paychecks while generating additional funding.

Backers of revenue based options often frame the solutions as ways to preserve scheduled benefit levels while minimizing immediate impact on take-home pay. However, they can also affect labor costs, compensation planning, and workforce budgets. For plan sponsors, understanding these possibilities helps put potential changes into context as Congress evaluates how best to strengthen the program’s finances.

Another set of proposals focuses on changing how Social Security benefits are calculated or when they are paid. These ideas aim to better align the program with longer life expectancies and current workforce patterns. In most cases, these changes would be phased in slowly and apply primarily to younger workers, rather than current retirees.

- Increasing the full retirement age

- Slowing benefit growth for higher earning workers

- Making changes to how annual cost of living adjustments are calculated

While benefit adjustments can improve long term sustainability, supporters also see them as a way to modernize the program in light of longer life expectancies. Critics argue that reducing scheduled benefits, especially for future retirees, shifts more responsibility onto individuals and employers to make up the difference. Discussions of possible changes can influence when people expect to retire and how much they believe they will need to save through employer sponsored plans.

Recently, some policymakers have proposed altering how Social Security’s reserves are managed to help improve long-term sustainability. These ideas focus on supplementing the existing trust fund with diversified investments, rather than relying exclusively on U.S. Treasury securities.

Some proposals would allow a portion of Social Security assets—or a new, separate fund—to be invested more broadly, similar to how some large public pension plans invest their reserves. One bipartisan idea discussed in Congressional hearings would create a supplemental investment fund, initially seeded with federal dollars, and managed independently with a long term investment horizon. The goal would be to use higher expected returns to help close part of the financing gap over time, without immediately increasing payroll taxes or reducing benefits.

Advocates contend that carefully governed, long-term investment strategies may improve outcomes without immediate tax increases or benefit cuts. Skeptics, however, raise concerns about market risk, governance, and whether investment returns should play a role in funding the program.

While these proposals remain debated and face political and practical hurdles, their inclusion in current policy discussions reflects a broader reassessment of how Social Security can be updated for a different economic environment than the one in which it was created.

Historically, major Social Security reforms relied on a mix of revenue increases and benefit adjustments rather than a single change. Most analysts expect the same approach this time.

For plan sponsors and financial professionals, the exact policy outcome matters less than the broader direction: Social Security will continue to play a foundational role in retirement income, but future benefits may look different than participants expect under current law.

That uncertainty reinforces the importance of employer sponsored retirement plans in helping workers prepare for retirement income beyond Social Security alone regardless of which specific policy mix Congress ultimately adopts.

Recent Congressional hearings and policy analyses highlight the importance of bipartisan cooperation, as no single lever fully closes the financing gap on its own.

For plan sponsors, Social Security reform is not an abstract policy issue. It influences:

- Retirement timing expectations

- Confidence in claiming strategies

- Contribution adequacy in workplace retirement plans

- Demand for lifetime income solutions

Uncertainty around Social Security can lead participants to delay decisions or underestimate the role that employer sponsored plans play in long term security. Clear, fact based communication that emphasizes that Social Security will continue but isn’t intended to be a complete retirement solution can help counteract misinformation and increase confidence.

While the timing and details of Social Security reform remain uncertain, understanding the potential paths forward helps plan sponsors better support participants and long term workforce planning. Your Principal® representative can help you put these developments into context, assess the potential changes to your retirement program, and identify strategies to support participant retirement readiness, regardless of how policy discussions evolve.