A nonqualified deferred compensation (NQDC) plan is a special benefit that helps key employees like you save more, manage your taxes, and retire on your schedule. Use these resources to learn about plan features, benefits, and considerations.

- A nonqualified deferred compensation (NQDC) plan is a type of plan employers put in place to reward key employees like yourself.

- It allows you to save additional pre-tax dollars beyond qualified retirement plan limits.

- You defer a portion of your compensation today that will be paid out later.

Explore these short videos that can quickly get you up to speed on all things deferred comp—including NQDC basics, how deferred comp could help you manage your taxes, what to expect when you enroll in a plan, and more.

| Feature | 401(k) Plan | NQDC Plan |

|---|---|---|

| Contribution limits | Contributions capped at the yearly IRS limit. | Contributions aren’t capped. |

| Tax-deferred status | Pre-tax contributions and investments earnings are tax-deferred until distributed. | Contributions and investments earnings are tax-deferred until distributed. |

| Access to your money while employed | Depending on the plan, a loan may be available, which must be repaid with interest. | Unscheduled withdrawals are not permitted. |

| Distribution options | Lump sum or partial payments. If distributed before 59½, a 10% penalty may also apply. May be “rolled over” into an IRA or other qualified plan within 60 days following distribution. | Could be lump sum or installments. Dependent on plan design and the type of distribution—separation from service or specified date. |

| Investments options | Offers a variety of investment options. | Offers a variety of investment options through reference investments. |

| Risk | Investment risk based on fund selection and market performance. Balances are secured from creditors in the event of company bankruptcy. | Investment risk based on fund selection and market performance. Investment risk based on fund selection and market performance. |

- Save more. Deferred comp can help you save beyond the limits of qualified plans like a 401(k). And pre-tax deferrals result in tax-deferred growth, allowing compounded earnings to help you save more.

- Manage your taxes. Deferring a portion of your compensation reduces your taxable income. And you’ll have more control over how and when you pay taxes on what you saved.

- Retire on your schedule. With no age-based rules on when you receive deferred comp income, the plan could potentially help you retire early.

- Can you afford to defer a set amount of income for the entire year—with no loan or withdrawal?

- The amount you defer is locked in for the year and you don’t have any loan or withdrawal options. So it’s important to save what you can afford.

- If your needs change and you need to reschedule a distribution, you must let your employer know at least 12 months before the scheduled payout (no changes are allowed within a year of your scheduled distribution). The payout also must be delayed at least five years from the originally scheduled distribution date.

- Are you maximizing your qualified plans?

- If not, do that first and use catch-up contributions if you’re age 50 or older.

- Savings in qualified plans like a 401(k) plan are yours and protected from creditors by the federal law.

- Keep in mind that deferred comp deferrals reduce the income available to contribute to a qualified plan.

- Note: You can’t roll money over from a qualified to a nonqualified plan.

- Do you want to lower your tax rate?

- If so, a nonqualified plan can help.

- Distributions are treated as ordinary income when they’re paid out, and they’re subject to current federal and state income tax.

- Are you concerned about meeting your retirement savings goals?

- If so, the NQDC plan can supplement your other savings plans.

- If not, deferred comp could still help you meet other financial goals.

- Are you confident in your employer’s success?

- Nonqualified plans have fewer government-imposed restrictions than qualified plans, but they don’t have the same government protections.

- Some plans place deferred compensation in a trust, which is used to hold assets and pay benefits. While your employer retains control of any deferred money until it’s paid out, the trust protects you from a change of control in company ownership. It also protects you from a later change of heart by your employer—after you’ve deferred income but before it’s paid out.

- The only situation where your company’s promise to pay out deferred compensation could be broken is if they became insolvent or went bankrupt. Then, the bankruptcy process would determine how or if you’d get paid.

Distributions, or payouts, are how you receive money from your nonqualified deferred compensation plan.

- The distribution is dependent on the type of account or goal you’ve set up for your plan:

- Retirement. A retirement account pays out once you leave your employer, regardless of age. It can help replace your income after you’ve stopped working but before you start drawing down other retirement savings.

- Savings. A savings account, also known as an in-service account, is designed to help meet short-term goals such as paying for a college education or second home. These accounts generally pay out while you’re still working, and you choose how and when to receive the distribution.

- Distributions occur depending on your employer’s plan design. The money is paid out in lump sums or installments.

- Depending on how your employer set up the plan, installments could be paid out annually, semi-annually, quarterly, monthly, bi-weekly, or weekly.

- Events both in your control (such as leaving for a new job or retiring) and out of it (like death or a disability) can trigger distributions.

- Decisions made when establishing accounts during the enrollment process determine how the accounts distribute.

- You’ll pay federal income taxes on the amount paid out, along with any applicable state taxes, the year you receive your distribution.

- If deferred income is needed unexpectedly, circumstances like death, disability, a change in company control, or financial hardship may qualify you to receive this money outside of when it was planned to be distributed. During enrollment, you designate how to receive your money from the plan should one of these situations occur.

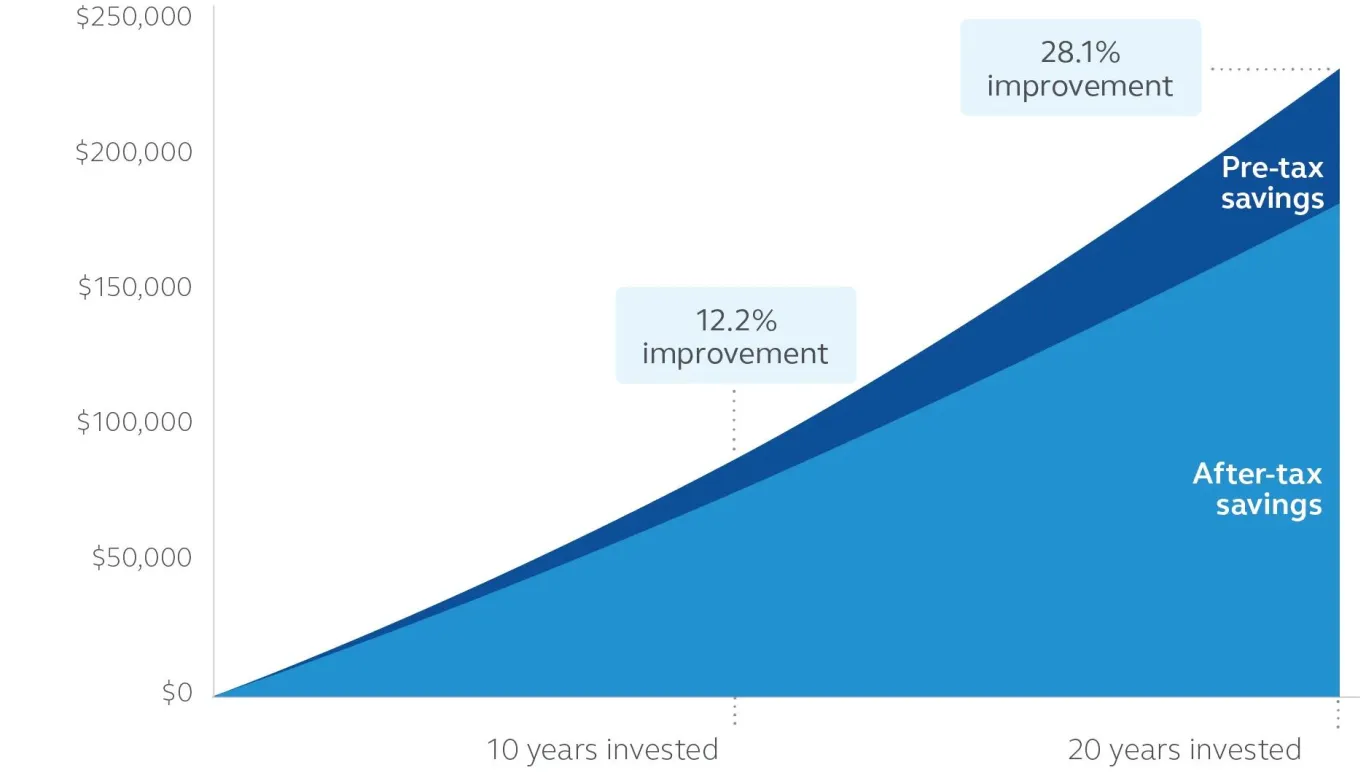

Thanks to compound interest, the tax-deferred advantage increases the longer you let your balance grow. The example below1 shows that over time, assuming the same earnings rate, you’d have a larger account value from a pre-tax investment.

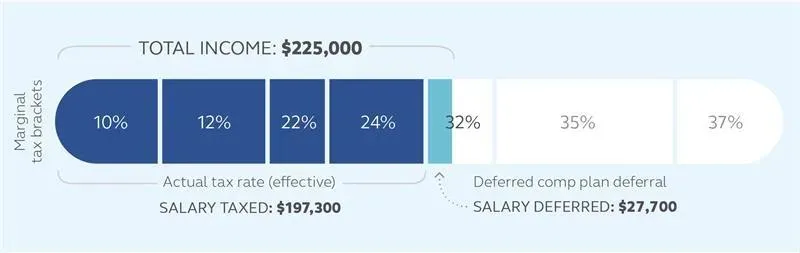

- With a deferred comp plan, you can also defer your highest tax bracket income to help lower your actual tax rate.

- Each dollar is taxed at the rate of the tax bracket it falls into. The first dollars you make are taxed at a lower rate, and the last dollars you make are taxed at the highest tax bracket you reach. These are called marginal tax rates, and there is a different rate for each tax bracket. Your average or combined tax rate is called your effective tax rate.

- Preventing money from being taxed at the higher marginal tax rates will lower your effective tax rate, like in the example below.

- You pay income taxes when you receive the money you’ve deferred. Depending on when you receive your payout, you could lower your annual taxable income enough to drop into a lower tax bracket in your retirement years.

- Keep in mind that distributions from a nonqualified deferred comp plan are treated as ordinary income, and are subject to current federal and state income tax.

1 The illustration is a hypothetical example showing the principle of compounding. This example assumes an initial investment of $10,000 with ongoing annual contributions of $10,000 growing at an annual 6% rate of return compounded annually over a 20 year period. The example does not include the impact of any fees and expenses that would be associated with an actual investment. It does include a lump sum distribution of the pre-tax amount with a 40% tax rate. This hypothetical illustration is not intended to represent any specific type of investment. Keep in mind there is no assurance the investment will grow at a steady rate of return and consumers need to consider their personal investment horizon and income tax bracket, both current and anticipated when making investment decisions as these may further impact the results of the comparison.

- Rather than investing directly into funds, nonqualified plans use “reference” investments—a plan requirement to help preserve the tax-deferred status of the plan.

- You can direct your deferrals toward a variety of reference investment options that align with your risk profile.

- Reference investments you select may or may not actually be selected by your employer.

- A reference investment mirrors the performance of an actual investment and is used solely for the purpose of calculating earnings.

- Any potential growth or loss is determined by the performance of the reference investment you chose.

Learn more about how NQDC distributions work.

Distributions are triggered by events:

- Within your control, like leaving an employer for a new job or due to retirement.

- Out of your control, such as a death, disability, change in the company’s control, or financial hardship.

The money in your plan will pay out based on selections you made when you enrolled.

You’ll pay federal income taxes on the amount paid out, in addition to any applicable state taxes.

If you have an in-service account, which can also be called a savings account, the earliest you can take a distribution from this account is two years after you make your first deferral.

- Keep in mind, if you leave your employer before your account has finished paying out, you’ll receive the money according to selections you made when you set up the account during the enrollment process

If you have a retirement account, this distribution would trigger when you leave your employer.

- Lump sum. You get the entire account balance on a date you’ve selected.

- Installments. You get a portion of the balance at a time you’ve chosen, and what remains in your account has potential to continue growing tax-deferred.

- For example, you could have annual installments from your account paying out around each valuation anniversary for five years.

The amount you’ll receive is based on how much is in your account and how you’ve set up the money to be distributed. The amount in your account reflects contributions plus any compounded earnings.

You can change your distributions by delaying when you receive them. This is called redeferring.

You’ll need to follow the 12-month, 5-year rule:

- You need to request a change to your distribution at least 12 months prior to the currently scheduled payout date.

- The payout must be delayed at least five years from the currently scheduled distribution date.

- You won’t be able to make a change within 12 months of the scheduled distribution date.

- Changes can be made during the open enrollment period for the plan. The changes will be effective the first day of January.

- Your elections will continue in effect for the calendar year, or until you are no longer an active participant in the plan.

The types of accounts you have are dependent on what your employer allows. There are two main types:

- Retirement. A retirement account pays out once you leave your employer, regardless of age. It can help replace your income after you’ve stopped working but before you start drawing down other retirement savings.

- Savings. A savings account, also known as an in-service account, is designed to help meet short-term goals such as paying for a college education or second home. These accounts generally pay out while you’re still working, and you choose how and when to receive the distribution.

Note: Separating from the company may be an intervening event into a savings goal. Depending on the company's plan structure, when making a Separation from Service election during enrollment, you may either apply one separation choice to all accounts or select different options for each individual account.

Learn more about the

- Deferred comp plans use reference investments, which don’t invest directly into funds. Reference investments track alongside real investments (like stocks, bonds, or mutual funds), and they’re used solely for the purpose of calculating earnings.

- Any potential growth or loss is determined by the performance of the reference investments you chose.

- Reference investments help determine:

- How your deferred money grows over time.

- What your eventual payout will be.

- How market performance affects your deferred compensation.

- For example, if you choose to reference a mutual fund that grows by 10%, your deferred money would grow by 10% too, even though no actual investment was made.

- Reference investments help preserve the tax-deferred status of the deferred compensation plan.

Your employer chooses the reference investments available for the plan. You can change your investments at any time by

No, deferred comp can’t be rolled over.