Discover how the cost of delayed retirement affects both office and production workforces and explore how automated plan features can help each group retire on their own terms.

A large manufacturing organization began to see a growing disconnect between when employees wanted to retire and their financial readiness to do so. More employees, both office and production, were continuing to work past age 65. Some did so because they wanted to keep working, but many simply didn’t feel financially prepared to stop working. Over time, this pattern created broader workforce challenges, including slower succession, fewer advancement opportunities, and rising employment costs associated with longer-tenured roles.

It’s important to note that many of these employees with deep experience continued to be an asset to the organization, enhancing quality, training, and continuity, even as leaders recognized the importance of helping them retire on their preferred timeline.

Principal® analysis shows that in labor-intensive industries such as manufacturing, the estimated annual cost per employee age 65 and older exceeds $93,000.

Many organizations often support two very different employee groups: office and production workers. These roles differ significantly in physical demands, wage progression, and career longevity, which shape when and how they can retire. Introducing a dual-workforce perspective into plan design can help account for how differently these groups experience work and saving.

Rather than viewing this solely as a retirement issue, the company’s leadership reframed it as a workforce-readiness challenge, carefully tied to how employees saved throughout their careers. A closer review of the retirement plan showed that while the retirement benefit itself was competitive, plan design elements such as default contribution rates, automated features, and engagement touchpoints were influencing whether employees were realistically ready to retire when they wanted to.

Guided by this dual-workforce perspective, the company evaluated which plan elements would best support each employee group.

Our advanced plan design modeling suggested that modest adjustments, particularly those that encouraged earlier participation and gradual increases in savings, may meaningfully improve retirement readiness. Equally important, the projected long-term employer cost of these changes was expected to be less than the average cost of a single year of delayed retirement for their employee population.

Understanding the distinct employee segments in a dual workforce is important for designing retirement plans that support retirement readiness, helping employees retire when they want while managing the cost of delayed retirement.

For plan sponsors seeking scalable ways to influence retirement outcomes, automated plan features tend to stand out for their consistent impact on participation and savings behavior. Rather than relying on individual action, these features help align employee behavior with long- term retirement goals.

Office employees. Office roles tend to have some of the highest per-employee costs when retirement is delayed. Because the work is typically less physically demanding, employees can often continue in these roles longer with elevated compensation and benefits.

Such workers may see their compensation rise significantly as they advance. Since qualified retirement plans have strict contribution limits, top earners may struggle to accumulate enough to replace a large percentage of their pre-retirement income if they didn’t start saving early in their careers.

For employees with higher earnings potential and longer careers, plan design may prioritize stronger early accumulation:

- Higher auto-enrollment defaults (such as 8%–10%) to reflect long-term savings needs

- Annual auto-increase to help keep pace with income growth and prevent stagnation

- A stretch match that encourages higher employee contributions, helping boost savings rates without necessarily increasing employer cost. Example: offering a 50% match up to 8% instead of a 100% match on 4%, so employees must save 8% to receive the full employer match.

- Immediate eligibility to capture early career saving opportunities

Production employees. Production roles often involve physical demands that can affect how long employees are able or want to continue working. This likely explains why the labor- intensive industry tends to have a smaller share of employees (6.4%) working beyond age 65 than other industries in the analysis.

For production employees, the retirement challenge is often less about late-career income growth and more about making the most of their active working years. When the savings window may be shorter, plan design plays a critical role in supporting early participation, appropriate contribution levels, and sustained engagement over time.

In roles with a shorter savings window, plan design can emphasize momentum and consistency:

- Auto-enrollment at a meaningful default rate (such as 6%) to establish a strong starting point

- Auto-increases of 1% annually (with flexibility to adjust to 2% for faster savings growth)

- Annual re-enrollment to help re-engage eligible employees who are not participating

- Lower the eligibility age and allow immediate eligibility to help maximize the savings window

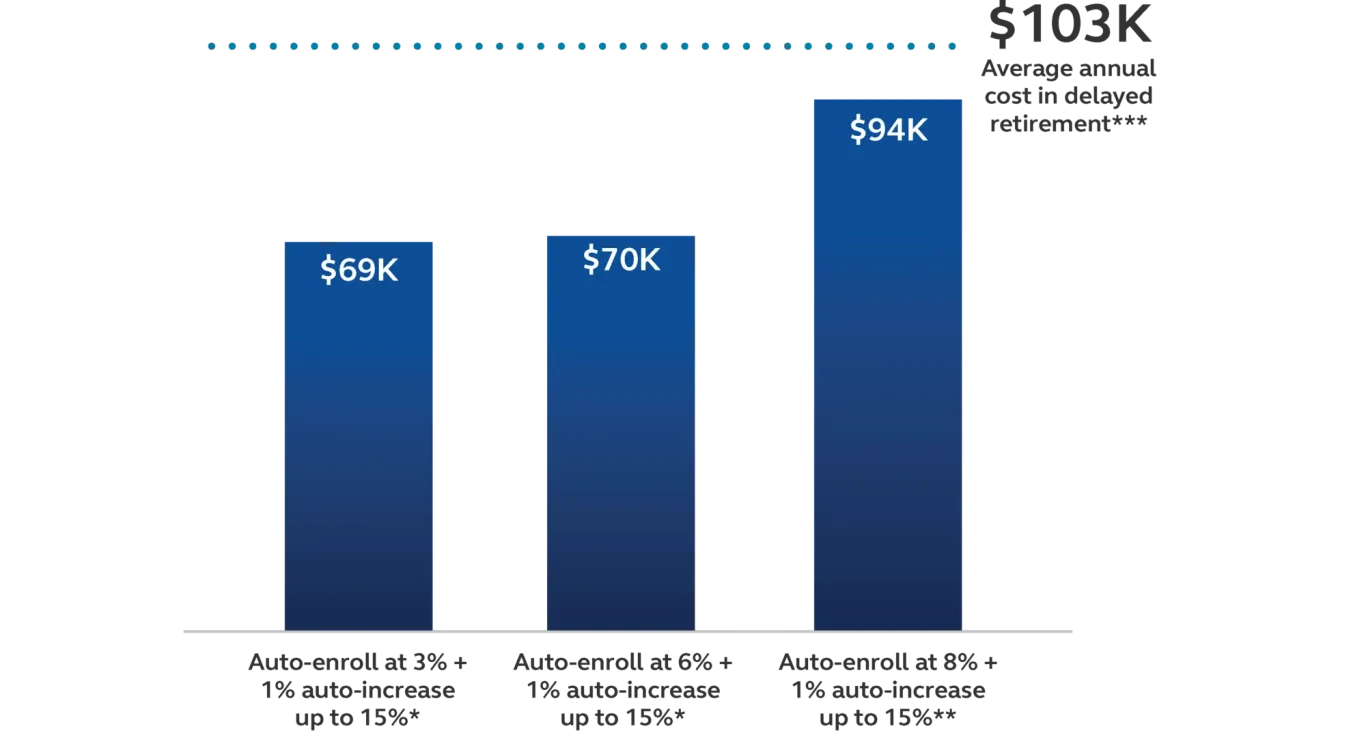

Implementing automated features can be especially effective at helping employees save what they may need to retire. While these features may require some upfront investment, they have the potential to generate significant long-term savings, especially when compared with the recurring annual cost of delayed retirement. Principal® analysis shows that when an employee works past age 65, it costs an employer an average of $103,000 per year in additional compensation and benefits, regardless of industry.

The chart below illustrates several automated feature options and their estimated costs. Beyond financial benefits, helping employees retire on time may contribute to workforce mobility, stronger morale, and greater team engagement.

Total employer contributions (in future dollars without earnings):

Many companies operate with two distinct employee groups, office and production, whose careers, savings patterns, and retirement timelines vary significantly. Instead of managing separate plans, employers can often support both groups through a single plan with strong defaults and automated features. This approach can create a consistent foundation for retirement readiness while helping reduce long-term workforce pressures and cost risks. With delayed retirement costing an average of $103,000 per employee per year across industries, proactive plan design may become a strategic advantage.

Ready to take a closer look at your retirement plan design? Your Principal® representative can help you assess how your current plan supports the retirement readiness of office and production employees. They can also identify thoughtful plan design strategies that align with your unique workforce, goals, and budget.