How plan sponsors can benefit from repairing participant data.

Key takeaways for pension plan sponsors

Just one inconsistency on a record within a defined benefit (DB) census file of hundreds or thousands is easy to ignore, like a slow dripping faucet. Plan sponsors know the problem is there but can easily choose to ignore it.

The consequences of this pension plumbing procrastination may be minor. Estimation techniques for actuarial valuation purposes usually address immaterial data omissions and inconsistencies. From an administrative perspective, the benefit calculation process would then reconcile the estimated data for each participant when they apply for their pensions.

Individually, these single drops of pension obligations have little weight, with no real attention paid to their shape or direction. When thousands of records come together, however, they combine into powerful cashflows. More than once, sudden downturns in bond yields have caused liability pipes to break and flood sponsors’ balance sheets.

Since pension liabilities are simply individual data records interpreted by an actuary as a financial obligation, understanding the unique risk characteristics and liquidity needs of each plan requires accurate data. Although it is tempting to leave fixing the data faucet drip for another day, there are three very compelling reasons for doing it now: cost, efficiency, and risk.

The result of most data cleanup projects is the discovery that current obligations are being overstated. A common reason for this is that plan sponsors are still accounting for pension obligations for deceased participants. Despite technological progress through the years to help account for this, the deaths of pensioners and their designated beneficiaries still often go unreported. Data repair projects often uncover a considerable number of unreported deaths, many from the population of vested terminated participants – those who are no longer employed by the company but accrued a pension benefit.

Unless verified, participants who are deceased remain in the plan inaccurately contributing to the plan’s overall liability total. The cost impact of correcting this overstatement is far reaching. Consider a hypothetical plan with a $100 million total liability. A 1% reduction due to removing twenty deceased records (which is not an unreasonable result) can have the following benefits to the plan sponsor:

- Immediate 1% increase in funding ratio.

- Minimum contribution reduction of about $100,000 annually.

- PBGC premium reduction up to $54,000 annually

This is the maximum savings using a 5.2% variable rate premium on $1m reduction to unfunded PBGC liability ($52k in savings) plus $2k in savings from the flat rate premium ($111 per person in 2026). . - Immediate $1 million balance sheet improvement.

- Immediate $1 million reduction to accumulated other comprehensive income (AOCI).

- Pension accounting expense reduction of about $50,000 - $100,000 annually

A $50k reduced interest cost on the liability (assume discount rate of 5%) plus another potential $50k for reduced amortization of AOCI from previous line. .

Above calculations done using Pension Protection Act (PPA) single employer funding and ASC-715 accounting rules.

Many plans today still operate under a “forensic reconstruction” administrative model, which pushes all validation, cleanup, and calculation work for each individual participant to when they file for retirement benefits. This can create several layers of effort that HR teams and consultants must work through manually and effectively becomes a custom audit for everyone.

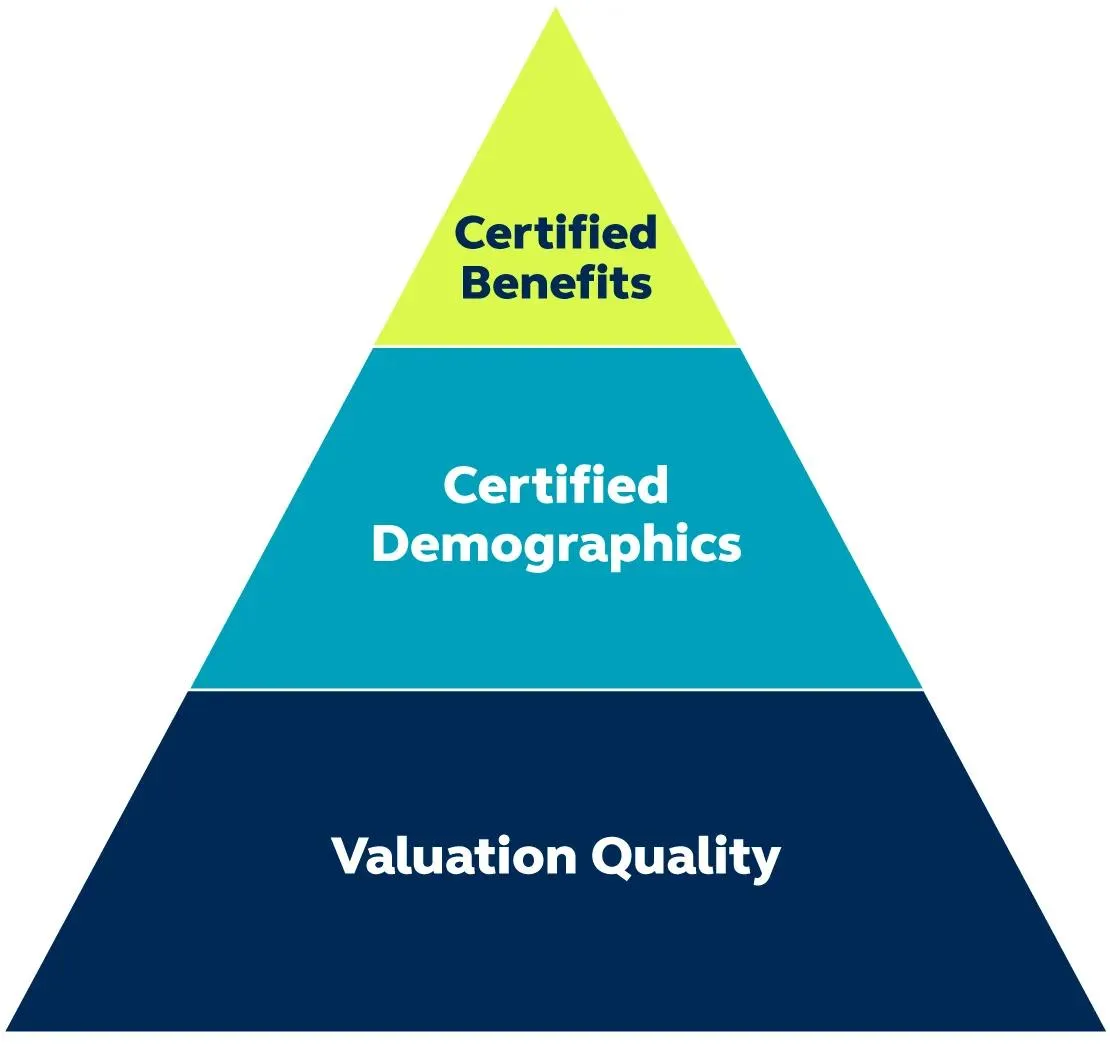

Completing a plan data review can significantly reduce the time and expense of administering pension events in the future. As shown in the graphic below, one layer of improvement could be to certify demographic data like birthdates, hire dates, death dates, and addresses. This is usually a simple project with lower cost to execute.

An additional layer of improvement would be certifying each participant’s pension benefit amount. This may require significant internal and external resources driving proportionally higher project expenses. Benefit certification may even be impossible if pay and service records are not available, as is often the case with larger plans aggregated through a series of mergers and acquisitions.

Ideally, both benefits and data can be certified and project costs offset by future savings from streamlined pension plan administration.

Accrued benefits recalculated and verified based on primary human resources data and plan provisions.

Key admin/communication fields verified:

- SSNs

- Birth and death dates

- Spouse information

- Mailing address

Adequate for actuarial valuation work.

Key fields for administration and communication often not current.

Benefits sometimes estimated.

While data repairing is not considered a “glamorous” initiative, the financial impact of small improvements can add up. Quite often, the cost savings realized can be significantly greater than the cost of the data cleanup project. Accurate and certified data can reduce costs, improve execution, and mitigate risks. So, it is time to consider grabbing a wrench and repairing that data drip.

Mike Clark is a fellow of the Society of Actuaries (SOA) and a member of the American Academy of Actuaries (AAA) with a master apprentice certification in pension data plumbing.

No matter where you are in your pension journey—from accumulation to hibernation or transfer—we offer tailored solutions for each stage.