Asset allocation helps to balance your investment choices to help you meet your goals and time horizon, as well as align with your risk tolerance.

Quick takeaways

You’ve probably heard the saying “Don’t put all your eggs in one basket.” It’s an expression that can apply to a key investment strategy, too: asset allocation. In investing, asset allocation is like making sure your eggs (in this case, your money) are in different baskets (your mix of investments from various asset classes). Doing so seeks to manage risk, maximize growth potential, and ultimately, may help achieve your financial goals. Here’s an asset allocation explainer.

Asset allocation is simply choosing investments from different asset classes. The three main asset types, or classes, are stocks, bonds, and cash (sometimes called cash equivalents, such as a money market). (See more on that below.) Your asset allocation can range from conservative (which typically has low risk) to aggressive (generally high risk). It’s often based on your risk tolerance and should align with the timing of your financial goal.

For example, let’s say you’re saving for a down payment on a home, and you hope to have enough in the next one to three years. You may want to limit higher risk investments but you also want the opportunity for some growth, so you might invest in a low-risk mix of cash, money market, and short-term bonds. On the other hand, if you’re saving for retirement and it’s decades away, you might invest most of your money in high-risk stocks, which can help increase growth potential. In this case, you may have time to weather natural market fluctuations.

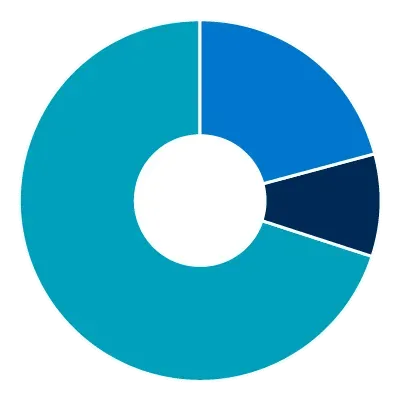

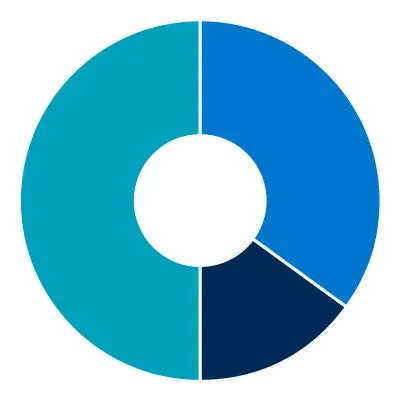

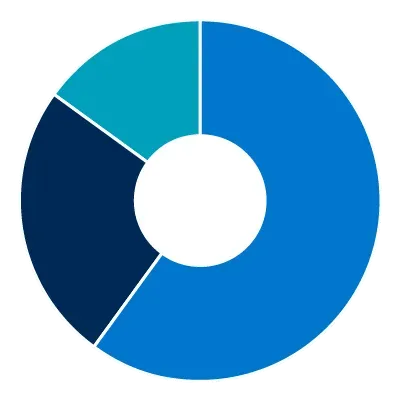

Here’s how different portfolios’ asset allocations might be structured based on investment risk:

More conservative

Balanced

More aggressive

There are several asset class types in investing. Within each class are many individual investments to choose from. Each asset class generally behaves differently when it comes to growth, stability, and liquidity.

| Asset class | What it is | Growth potential | Stability |

|---|---|---|---|

| Stocks | Shares of publicly traded companies | High growth; can earn a lot of interest over time, but can also have high losses | Highly volatile; may change value quickly and frequently |

| Bonds | Fixed income; loans to governments or companies | Moderate growth; can have less earning and loss potential than stocks, but more than cash | Moderately stable; less likely to fluctuate dramatically with the market |

| Cash or cash equivalents | High-interest savings accounts, money market funds, CDs | Low growth; can have more earning potential than a traditional savings or checking account, but non-bank products can still have a loss | Stable; an option for cash that isn’t needed for typical monthly expenses |

| Alternative investments | Funds outside traditional asset classes such as real estate (REITs), commodities, digital assets (crypto) | High variability; can have a wide range of outcomes due to complexity, availability, and differing regulatory requirements | Highly volatile; may change value quickly and frequently and could be illiquid |

Asset allocation is one of the biggest factors in determining the investment portfolio’s overall performance, or gains and losses. For instance, a portfolio that is 90% stocks and 10% bonds will likely see far different growth over a 20-year period than a portfolio that is 10% stocks and 90% bonds

Think of diversification as the next layer of allocation within your investment strategy. Diversification is the mix of investments within each major asset class—how much of stock A and stock B that you have. That can help reduce the risk that any one stock or bond could be the cause of a negative portfolio performance.

Diversification and asset allocation work together; not only is your money divided among asset classes, but it’s also divided within that asset class itself. By building your portfolio with a mix of asset types and with a mix of individual investments within those buckets, you may have a better chance to reach your financial goals.

When it comes to asset allocation and diversification, there is no one size fits all; there’s only the right mix for you. There are three important factors:

Your financial goals

What are you saving for, and how much will you need? It’s typical to have multiple financial priorities you’re juggling at the same time. Maybe you’re saving for a child’s education in 10 years, a new car in three years, and your retirement in 20 years. Start by setting a baseline for how much you can save toward each goal.

Your timeline

How long will it be until you want or need to use the money? If you have a longer timeline, you have more time for your money to grow and to recover from any market ebbs and flows. Conversely, if your timeline is short, you may choose to invest heavily in fixed income or money market funds, earning some interest but keeping your funds less exposed to volatility.

Your risk tolerance

What’s your comfort with market risk? There’s a balance between investing for potential gains and minimizing anxiety you may have with short-term market volatility.

Asset allocation is not a set-it-and-forget-it practice. Instead, aim to check your investment mix a couple times a year (possibly at your mid-year and year-end check ins) and consider making changes to better align with your goals. Talking with a financial professional may also help you feel more confident about your overall plan.

Login in to your account with Principal to check your investment mix and make updates if needed. On your dashboard, select your account(s) on the left-hand side. Then, click “Investments” on the top menu.