Investing in your retirement when you’re just starting your career can pay off, and these simple strategies may help you know what to do.

Turns out, when it comes to the advantages of saving early for retirement, many young people get it: 41% of people

And, it’s good news, too.

“Investing young, even if it’s just a small percentage of your income, does two things,” says Heather Winston, director of individual solutions at Principal®. “First, it establishes good savings habits that will apply universally, regardless of what your savings goals are. Second, the sooner you start, the longer your money has to grow over time.”

If you’ve already been able to save something, even a little, for retirement early in your career, congrats. If you haven’t yet, but want to join the ranks of the early investors, congrats are due to you, too. How do you start saving when you’re young, or ramp up what you’re contributing to make even more progress? We’ve got some suggestions.

No matter how old (or young) you are, you’ll always be juggling competing financial goals and priorities. Take student loans: About 25% of people under age 29 have student loan debt, as do 14% of those age 30-44 years old.

That juggling act may make you feel that what you can save is too small to be impactful. But it’s not. Why? It’s time in the market, not timing the market, that matters.

What that means is, historically over long periods, markets have grown. So, the earlier you invest, the more time you have to let compounding work for you. That’s true even if you invest while young and stop, versus invest for longer when you’re older. This chart explains what happens.

| Details | Saver 1 | Saver 2 |

|---|---|---|

| Initial investment age | 25 | 35 |

| Yearly investment | $12,000 | $12,000 |

| Investment length | 15 years | 30 years |

| Total invested | $180,000 | $360,000 |

| Total value at age 67* | $1,346,039 | $948,098 |

*Assumes 6% growth. This example is for illustrative purposes only.

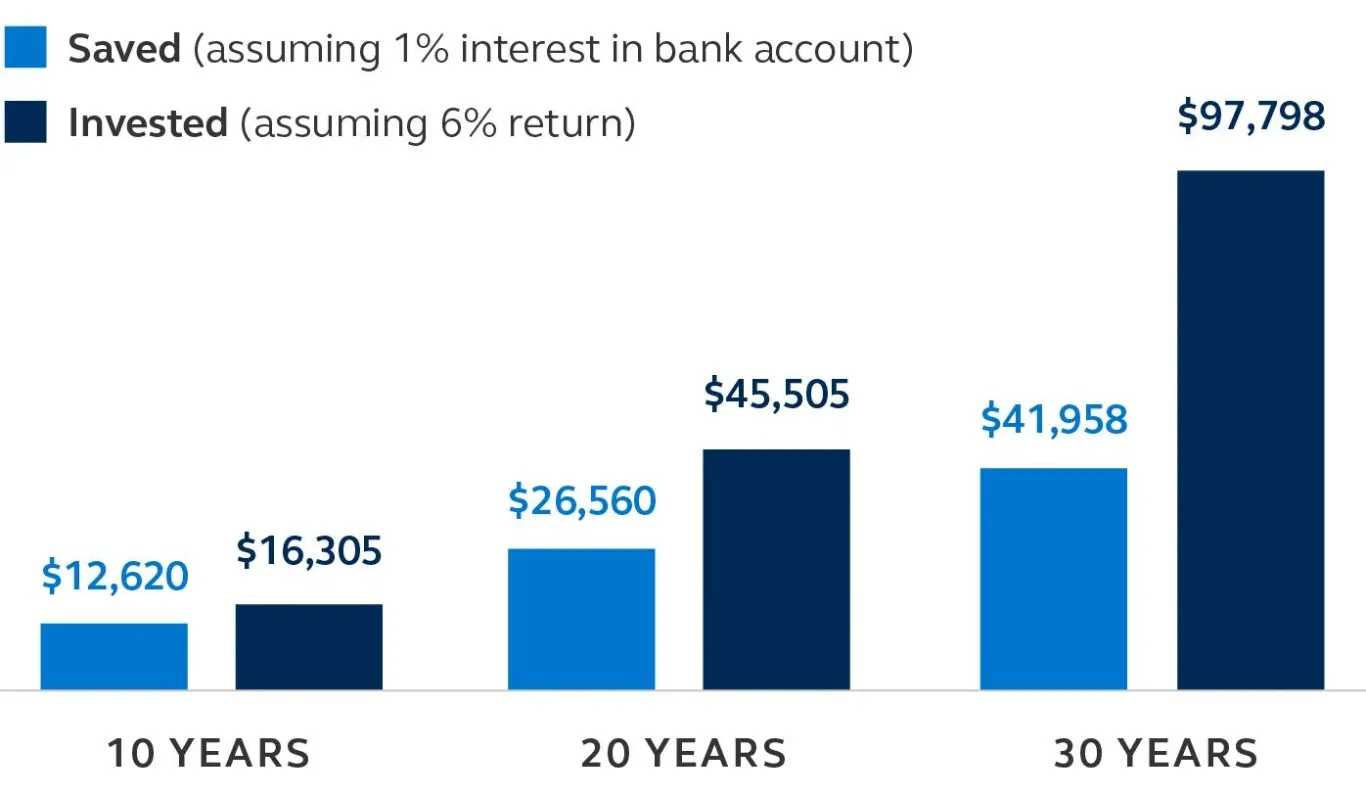

Let’s say you have been putting $25 a week in a traditional savings account, using an automatic transfer. You’re establishing a great habit, but your money isn’t working very hard. It’s probably only earning about .5-1% in interest, with little potential for that interest rate to change.

Contrast that with the same amount—$100 a month—put in a retirement savings account that’s tied to investments in the market. There’s more potential for your money to grow. Take this example: Even if you never increase the amount you’re saving, the growth in the investment-tied account versus the traditional savings account historically is more than double.

*Assumes $100 per month with 6% return. This example is for illustrative purposes only.

Although 73% of employees have access to a workplace retirement plan, only about half take advantage of saving in it.

If your workplace has an employer-sponsored retirement savings plan, auto enroll is an easy way to just start saving, even a little. If you can, save enough to get an employer match, if offered; it’s a quick way to boost your savings rate.

Does auto enroll make an impact on retirement savings preparedness? In a word: Yes—especially if you’re younger. For those who can use auto features like auto enrollment, retirement savings shortfalls decrease by a whopping 60%.

Nearly every retirement savings company offers an app to track contributions, manage beneficiaries, and more. And, they’ll often include helpful tools that you can use to try to build your financial foundation. (At Principal.com and on the Principal app, you’ll find a budgeting tool after you log in.)

One idea if you pay off debt? Think about diverting that same amount into retirement savings, if your budget allows.

Not everyone has a retirement savings plan through their workplace. Or, they may be self-employed and not sure where to start. There are options, though, and many of them work well for early-career savers.

For starters, you can open your own Roth IRA, any time, as long as you meet certain income limits. Roth IRAs are created with after-tax contributions, meaning you’ve already paid income tax on those dollars. So, when you withdraw them in retirement, you won’t have to worry about a tax bill.

You can also save in a traditional IRA on your own; unlike a Roth IRA, these use pre-tax funds (and you may be able to deduct contributions, too). You’ll pay the income tax on a traditional IRA when you make withdrawals in retirement.

There are a couple of reasons to think about adding both of these tools to your early investing strategy. For starters, both travel with you no matter what job you have. So, you can add to them even if you’re already saving in a 401(k). And, if you leave the workforce but are able to save, you can add contributions, within any IRS-defined limits, as you’re able.

When retirement is decades away, saving for it might seem like a tomorrow problem, not a today problem. But starting your investing strategy early helps you focus on your financial goals, no matter how much they change.

“Envision what you want your future life to look like and what you’re willing to do to attain that,” Winston says. “Life will bring twists and turns, and those events will change how you prioritize your goals along the way. It is common to make tradeoffs over long-term goals. Keep your goals simple to create consistent behaviors and positive habits—and help control the amount you save as you go.”

Want to analyze your budget to try to figure out how to save for retirement? Try our interactive budgeting and financial goals worksheet to review expenses, as well as set short-, mid-, and long-term goals.