The key findings from this year’s study prove continued value and need for deferred comp plans.

Despite the changing economic landscape, plan sponsors and participants remain certain that nonqualified deferred compensation plans provide value in retaining top talent and helping them save for retirement. In fact, 86% of plan sponsors offer deferred compensation plans to provide a competitive benefits package for key employees. And 90% of key employees consider a nonqualified plan important in preparing for retirement.

Additionally, both plan sponsors and participants agree that robust support matters when educating on the importance of this plan, and having access to resources when questions come up. 59% of employers are looking to financial professionals as essential partners in participant education. And two-thirds of employees value having clear access to plan support resources from the provider.

Those are just some of the insights from our latest deferred comp study.

Our annual deferred comp research can help you benchmark against your peers and gain valuable learnings.

Retention of key employees remains top of mind to employers.

76% of employers stated the top reason they offer deferred compensation plans is for use as a retention tool. This reiterates the importance of the plan when more than 50% of employers stated that it can be difficult to hire key employees with the right skillset. To help combat this challenge with recruitment and retention, 43% of plan sponsors also offer employer contributions in their nonqualified plan.

And 53% of employees agree that a nonqualified plan is important in deciding to stay with their current employer.

| Key reasons why employers offer a nonqualified plan | |

|---|---|

| Ranking | Reason |

| 1 | Provide a competitive benefits package for key employees (86%) |

| 2 | Help participants save for retirement above qualified plan limits (80%) |

| 3 | Retention tool for key employees (76%) |

| 4 | Help key employees manage current taxation (72%) |

By far, key employees’ number one reason for participating in a deferred compensation plan is to prepare for retirement. And 90% of plan participants say a nonqualified plan is important in helping them reach their financial goals for retirement. In fact, participants find the plan so valuable that 81% plan to either keep or increase their contributions during their next enrollment.

86% of plan sponsors agree that the reason they offer a deferred comp plan is to help participants save for retirement above qualified plan limits.

Employees’ reasons for participating in the plan can also help beyond retirement planning.

| Why employers offer a nonqualified plan | |

|---|---|

| Ranking | Reason |

| 1 | Save for retirement (68%) |

| 2 | Reduce my current taxable income during working years (14%) |

| 3 | Employer makes contributions I'd miss out on otherwise (14%) |

| 4 | Save for financial needs while I'm still working (4%) |

Both employers and employees agree that strong support matters when educating on the importance of a nonqualified deferred compensation plan.

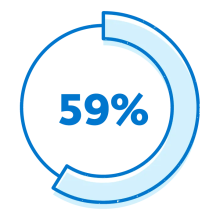

Financial professional support

59% of employers look to their financial professional for help with participant education

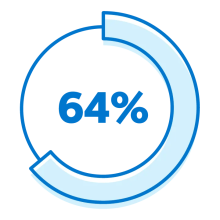

Plan sponsor support

While 64% of employees find value in clear access to plan support and resources

Talk to your financial professional about incorporating—or improving—a deferred comp plan in your benefits program.

Learn more about how nonqualified deferred compensation plans can help recruit, retain, reward, and retire key employees.